This blog was originally published in February 2020 and has been updated for our current financial climate.

We've updated our no-fuss guide to family budgeting to help you stay on top of your finances. Just because the world has gone crazy, doesn't mean your finances have to!

First things first, schedule a monthly budget meeting

Setting some time aside where you can focus on your finances without interruption is key. This can be extra challenging while sheltering in place. We suggest a budget date after the kids are asleep, or while they're watching a movie in the next room. (Although maybe not Frozen - all the singing that goes along with it could prove distracting.) Whatever you do, make sure to commit to a time where you can give your finances your full attention.

While the idea of talking finances with your partner might fill you with dread, we promise that regular conversations about financial planning will actually alleviate a lot of the stress around the topic. Go into the meeting with an agreed upon agenda so that everyone involved can come prepared. Bringing a positive and collaborative attitude about the future helps to minimize friction. Bringing snacks also helps - no one likes budgeting when they're hangry.

Identify your goals

Every family is different and there's no one-size-fits-all approach to family finances. A good place to start is to

identify your goals. Also remember to think about your goals from a perspective of needs versus wants. You

need to save for emergencies like a burst water heater, or say, a global pandemic. You

want to go to Hawaii.

Are you still struggling with your own student debt and a pesky credit card or two? If so, you'll likely want to prioritize debt repayment. Do you have the equivalent of 6 months of your income saved for emergencies? If not, now may be a good time to focus on building your emergency fund. If you have your debt and emergency fund under control and are looking to build wealth; identifying opportunities for investment might be your goal.

Discuss this together and then use the tips below that are relevant to you as stepping stones toward that goal.

Leverage Debt Freezes

It was just announced that the freeze on the interest and payment of federal student loans has been extended to September 30th, 2021. There's lots of talk about potential student loan forgiveness, but we still don't know if and when that will happen, nor do we know the conditions of forgiveness. So for now, it's best to stay on track with your student loan plan, whether that is repayment or forgiveness. On the plus side, the pause in payments and interest with give you some extra room in your budget

For example: If you usually pay $100 in student loan repayments a month, and student loan interest and repayments have been suspended until September 30th 2021, that means this year you'll have 9 months where you don't have to make a payment, which will total $900 plus all that interest you won't accrue. If that money isn't already spoken for, this could be a good opportunity to beef up your emergency fund, add to your investment account, or any other financial goal you have been eyeing.

Create a basic budget

Decide on a budget tracking method that everyone involved can understand and access. Whether you use a shared spreadsheet, a notebook, or an app is totally up to you. Not sure where to start? We've created this

simple budgeting spreadsheet template which makes it really easy to see where your money is going each month. (Don't have Excel? You can open this spreadsheet using Google Sheets.)

Begin by listing your monthly income, and then subtracting all of your monthly expenses, debit orders, and debt repayments. Don't forget to list all of your subscriptions, like Netflix, Amazon Prime, and the various apps on your phone. Go into the app store and see which apps you've subscribed to that have recurring charges - chances are, you could probably cancel some of those subscriptions right then and there.

Walletfi is a handy app for managing subscriptions and recurring charges.

Identify fixed expenses (ex. rent) and variable expenses (ex. groceries). Understanding how your variable expenses can change from month to month can help you better prepare for a more expensive month.

Listing out your expenses will give you an idea of how much money is left at the end of the month to put towards your main budget goal, as well as putting aside money to a 'slush fund' to help you avoid paying with credit when you have a month with higher variable expenses.

Prioritize paying off debt (If you don't have debt, work on not accruing debt)

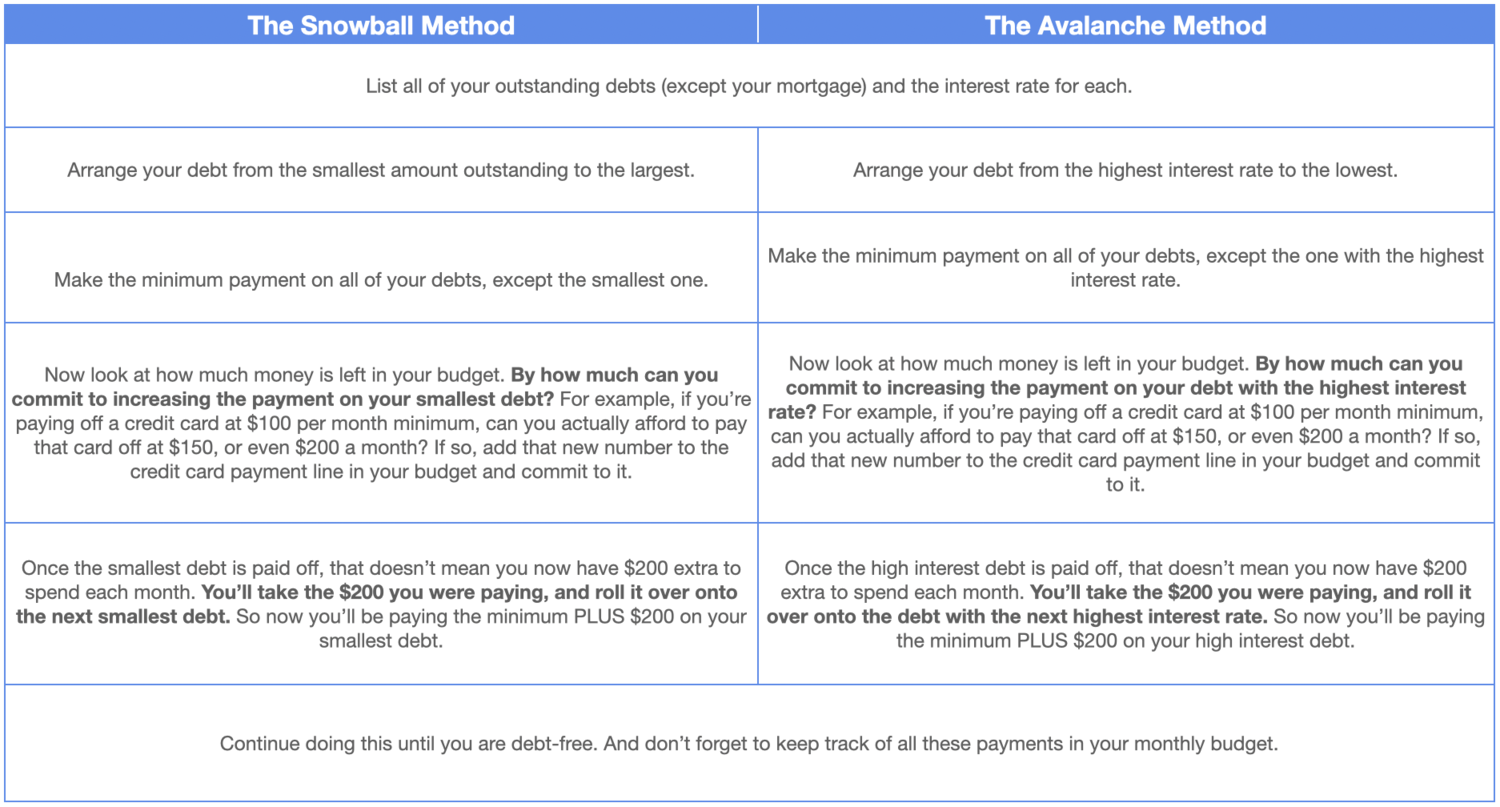

Take a look at your debt and decide whether it makes more sense to use the Avalanche, or the Snowball method to tackle your debt. The main difference between these two methods is that the Avalanche tackles the debt with the highest interest rate first, helping to minimize your interest paid over time, whereas the Snowball tackles the smallest debt first, helping you to see progress quickly, keeping you motivated.

The Avalanche makes a lot of sense, especially if you're paying off a credit card with a high interest rate, but as with anything, it's only effective if you do it. So if you're the type of person who needs to see noticeable progress to stay motivated, or if all your debt has very similar interest rates, the Snowball might be for you.

Plan for your child's future

If you have kids it's never too early to start saving for college. If you don't currently have a line item in your family budget for college savings, take a look at what is left over after monthly expenses and commit to a manageable monthly deposit into a college savings account and add it to your budget. No amount is too small - these things add up over time!

Not sure how much you should be saving? Our

budget template includes a helpful college savings calculator. You can either start by entering in the tuition fees of your dream college and working out how much you need to save each month, or you can enter how much you currently have available and it will calculate how much you will have saved with consistent manageable deposits by the time your child goes to college. Check it out on the last tab of the

budget spreadsheet.

Pro tip: By using a state-run 529 college saving plan, you can save up to 6 times more money than if you use a regular savings account. If that's not enough to convince you, 529 plans have tax-free earnings and will have the least impact on your child's financial aid eligibility.

Shameless plug: Don't have a financial advisor? Not sure where to start? We've got you! Scholar Raise makes signing up for a state-run 529 plan super simple. In just 5 minutes you could be on your way to saving effectively for college and all you need is the information on your driver's license & your social security number. No advisor fees, no account minimums. You could even set up an account during your budget meeting.

Building Wealth

If you've got your debt and emergency fund under control, now's the time to think about building wealth. Try to allocate as close to 10% of your income as you can to a long-term savings/investing plan - add that amount to the investment line item in your budget. If you're still employed, now is a great time to set aside a little extra, since you're not spending as much on dining out, entertainment and your daily commute as you usually do.

Don't feel bad if you're still paying off some debt and are not able to save a full 10% right off the bat. As long as you contribute something to your investments each month. Once you've paid off your debt, you'll have a lot more money left to add to your investments.

If the current economic climate has you feeling gun-shy about investing, remember this advice from ElleVest's

Sylvia Kwan:

"If you had invested in the stock market from 1999 to 2018, and not touched it, your money would have tripled. But if you had traded in and out and had missed out on just the 10 best stock market days over that period - just 10 days - your returns would have only been half of that. People may think they should wait for a pullback to invest, but the data shows that historically, "time in the market beats timing the market." - Sylvia Kwan

If you aren't sure where to start,

ElleVest and

Betterment take the guesswork out of investing and are FAR more cost effective than a traditional financial advisor.

Pro tip: If you have a 401K with your employer, don't forget to ask about employer matching. Find out based on your tax margin, whether pre-tax (traditional 410K) or post-tax (Roth IRA) makes the most sense for you.

Setting Additional Financial Goals

If you have anything left over at this point, you can start setting additional financial goals that make sense for your family. Don't forget to consider want vs. need!

Family vacations may seem like a distant memory at the moment, but things will normalize, and you'll likely be itching to travel by the time they do. Vacations toe the Family vacations may seem like a distant memory at the moment, but things will normalize, and you'll likely be itching to travel by the time they do. Vacations toe the line between need and want, as they are a great way to spend uninterrupted quality time together and make lifelong memories - but you don't need to travel somewhere exotic to do that. Besides, with all the changing travel restrictions in various countries, and new waves of the pandemic cropping up, you also might not feel comfortable traveling abroad yet. A trip to a local cabin, or even doing a house swap with a relative who lives in another town could be just as fun, could make your family feel safer, and might be a better fit for your budget for the time being. Maybe that trip to New Zealand can become a longer-term savings goal instead?

Same goes for cost-prohibitive extracurriculars for you and your kids. Of course you want the best for your family, but living beyond your means to send your child to a socially distanced equestrian camp, or for you to take up vintage car restoration is not a smart idea. If your interests are beyond your budget, that doesn't make you a bad parent. For the time being, look into online classes and YouTube tutorials that could teach the basics and some theory about your interests. Once things open back up, look for creative ways in which you can begin to expose your family to the things they're interested in without breaking the bank. Volunteering, open-days, community events, and work trade opportunities (if your child is old enough) are all great places to start. Always ask for scholarship or sponsorship opportunities.

Congrats, you've created a budget - now what?

Creating a budget is only helpful if you stick to it. To make sure you're getting the most out of your budget, be sure to take the time to balance it and adjust it as your needs change. Once you've followed our steps for creating a basic budget, you can continue to refine your budget monthly to make sure you can meet your financial goals.

If you find you're not meeting your savings or investing goals, a good first step is to separate your needs and your wants. Be really honest with yourself about your spending because no matter how much your kids need to watch Frozen 2 for the 100th time, Disney+ is still a 'want.' You don't have to cut everything out, but pay attention to the 'wants' included in your budget and figure out if there are any areas you could cut back or substitute with less expensive options.

Even if you are hitting every goal, this is a great way to check-in and see if there are any 'wants' that you don't really want, so you can shift that money to wealth creation, or things that actually bring you joy.

Next, it's important to update your budget with how much you actually spend compared to how much you budgeted. Our budget template lets you easily compare what you planned to spend vs. what you actually spent. Checking in frequently with your budget reminds you of your progress towards your goals, and tracking this information lets you fine-tune your budget month after month. It also helps you stay on top of any possible over-spending. If you are consistently spending more than you budgeted on groceries, you can take a look at those impulse purchases you made... did you really need 4 bags of Pirate's Booty just because it was on sale? If it's not impulse purchases, but truly a case of under-budgeting, you can tweak your budget to allow for increased spending on groceries while you cut back somewhere else.

The most important thing is to make sure your budget leaves some room for fun. You should still enjoy some 'wants' even if you are paying back debt or saving for financial goals. Maybe you won't make the trip to Arizona for a week at the spa, but you can afford a massage every other month if you budget efficiently. Budgeting for treats and things that make you happy will help you enjoy your hard-earned cash now, without adding to your debt and without taking away from your financial future.